What are Personal Capital and Mint?

Personal Capital and Mint are free online tools that can help you save time and optimize your financial life. They are often compared because they are both valuable personal finance tools.

Personal Capital is a free tool that syncs your accounts in one location and monitors your spending, net worth, and investment portfolio. It also provides wealth management services for a fee.

Mint is a free budgeting, spend tracking, and credit monitoring tool that helps you better manage money in your daily life.

Similarities: While Personal Capital and Mint are different tools, they have some similarities. They both do the following:

- Bring multiple accounts together in a single dashboard

- Track your spending and saving

- Flag changes in your financial accounts

- Provide specific insights you can adopt to improve your financial life

- Enable useful analytics and visualizations

- Offer multi-factor authentication

Differences: these personal finance tools differ in a few important ways:

- Personal Capital can help with investment analysis and forecasting with features like asset allocation breakdowns and investment fee analysis.

- Personal Capital can help with retirement strategy and planning

- Personal Capital can connect you with a real person for financial advice and wealth management

- Mint has the most robust notifications for day-to-day money management and monthly budgeting

- Mint offers free credit monitoring

- Mint only has an FAQ page, no human support

Why use Personal Capital or Mint?

Personal Capital and Mint both provide valuable information about your cash flow, investments, and spending.

They will both:

- Allow you to see your financial accounts all in one place

- Send automatic reminders when bills are due, fees get charged, or your spending behavior changes

- Provide insights based on your habits or goals

Offering personalized guidance tailored to your unique financial situation, Mint and Personal Capital can help you better understand your finances, ultimately increasing your wealth-building potential.

To get the most out of Personal Capital and Mint, you should plan around what each tool is built for and how it relates to your financial goals. For instance:

- If your concerns are around spending and saving, Mint may be the better choice

- If you want to ramp up your investing, Personal Capital has the edge

- You may also want to use both tools together to really supercharge your wealth-building ability

Here is a quick breakdown of what each platform offers:

Personal Capital is designed primarily for investment monitoring and management. Personal Capital offers a view of your investments at a glance—and analyzes your efforts to ensure you’re on track to meet your financial goals. You’ll see the fees and expense ratios your investments charge, so you can keep your investing costs low (a key component of building wealth).

Personal Capital’s insights can also help you diversify your investments, so you aren’t overly exposed to any one investment type. Personal Capital’s wealth management services combine human advice with robo-advisor based financial management.

Mint is designed primarily to manage your income and expenses. It acts as a budgeting tool by ingesting your checking, savings, and credit card activity to help you track where your money goes and monitor your spending habits.

You can visualize your spending by category, chart how your activity changes from month to month, or set up account alerts (such as a low account balance). Mint also shows your credit score free of cost and it does not have a paid version.

Side-by-Side Feature Comparison – Personal Capital vs. Mint

As you can see, while there is some overlap in the services each tool provides, they each excel in different areas. Together, they can be used to ensure you are on track for your goals and have a strong personal finance foundation and view of your financial accounts.

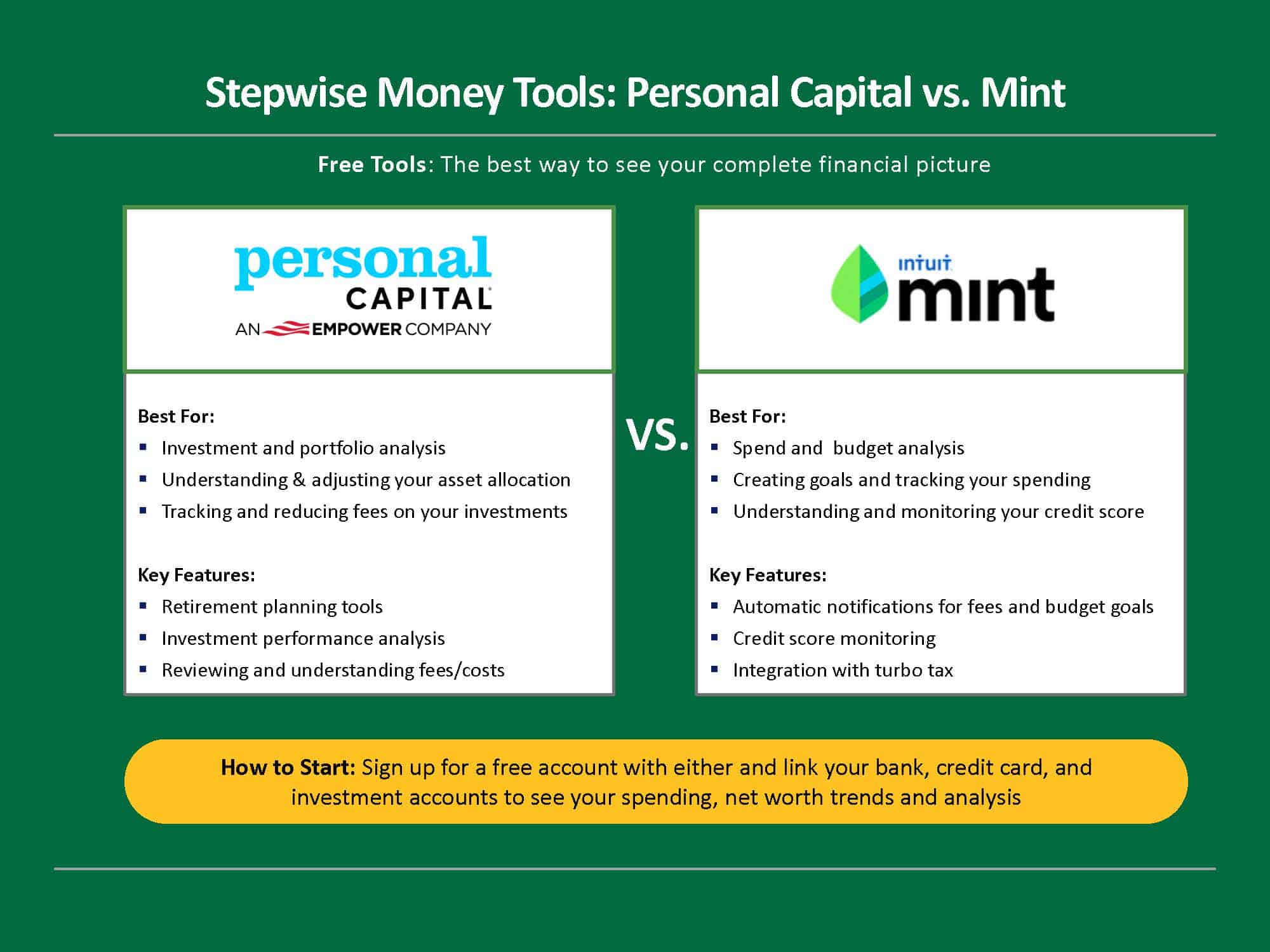

Personal Capital is best for:

- Net worth tracking

- Managing your investments

- Portfolio allocation recommendations

Mint is best for:

- Budgeting

- Spend tracking

- Monitoring your credit score

Here is a side-by-side comparison of each tool’s features:

| Does Personal Capital include this? | Does Mint include this? | Winner | |

| Investment analysis and monitoring | ✓ | ✓ | Personal Capital |

| Retirement planning | ✓ | Personal Capital | |

| Financial management | ✓ | ✓ | Mint |

| Budgeting tools | ✓ | ✓ | Mint |

| Net worth tracking | ✓ | ✓ | Tied |

| Credit monitoring | ✓ | Mint | |

| Pricing | Free | Free | Tied |

| Security | ✓ | ✓ | Tied |

| Bill alerts and management | ✓ | Mint | |

| Data synchronization for budgeting | ✓ | ✓ | Mint |

| Mobile app access | ✓ | ✓ | Tied |

| User experience | ✓ | ✓ | Tied |

| Customer service | ✓ | Personal Capital |

In-depth Feature Comparison – Personal Capital vs. Mint

Investment analysis and monitoring: Personal Capital has many superior features in this area. It is designed for viewing your individual investments and your overall portfolio, showing breakdowns of your assets, fees, and diversification.

- Winner: Personal Capital

Retirement planning: Personal Capital wins since your retirement strategy depends on having visibility into your investment, retirement portfolio, and savings on a single platform.

- Winner: Personal Capital

Financial management: Mint wins here by a narrow margin because it facilitates visibility into your savings and spending habits, which is the most essential element of better money management. If you aren’t saving enough, then it is impossible to invest.

- Winner: Mint

Budgeting tools: Mint has many superior features in this area, it can show you your spending by category as well as import and categorize your transactions. It also helps you set and monitor progress against a budget.

- Winner: Mint

Net worth tracking: Tied, they both do this well and show you the same core information from your accounts to track your net worth over time.

- Winner: Tied

Credit monitoring: Mint is the winner here, simply because Personal Capital doesn’t offer this feature right now.

- Winner: Mint

Pricing: Both are free to use for account monitoring and visualization. Mint doesn’t make money directly from you, only from affiliate marketing. Personal Capital charges fees on a sliding scale only if you decide to have them manage your money with the advisory platform.

- Winner: Tied

Security: Both use bank-grade security protocols and enable you to set up multi-factor authentication.

- Winner: Tied

Bill alerts and management: Mint offers alert automation, as well as more detailed transaction visibility. There are no alert features with Personal Capital.

- Winner: Mint

Data synchronization for budgeting: Mint has the edge here because it does a better job ingesting and categorizing your spending behavior. Personal Capital can be hit-or-miss in this regard.

- Winner: Mint

Mobile app access: Both platforms offer full-featured mobile apps for iOS and Android.

- Winner: Tied

User experience: Personal Capital and Mint have different use cases. The former is for investors and wealth management and the latter is designed for everyday personal finance tracking . But each one does its job well.

- Winner: Tied

Customer service: Mint directs you to a FAQ page for support, while Personal Capital offers help from real, live humans—usually within 24 hours.

- Winner: Personal Capital

Personal Capital Review

What is Personal Capital?

Personal Capital is really two separate services under the same brand name: a free investment management platform (which is what we’re talking about in this article) and a paid investment advisory service.

Free Investment Management Platform: When you use Personal Capital for investment management, it will bring all of your investment accounts into a single dashboard. You’ll also get lots of useful analyses and recommendations to help you balance returns and risk.

Its suite of tools includes:

- Portfolio Analysis: To understand how diversified your portfolio is

- Retirement Planner: To forecast how much you’re on track to save for retirement

- Retirement Fee Analyzer: To see how your account fees stack up to industry averages

- Investment Checkup: To gauge how your asset allocation compares to your goals and where you may need to re-balance

Paid investment advisory service: The investment advisory business is how Personal Capital makes money, and it’s only available to those with at least $100,000 to invest. They combine a human advisor service with a Robo-advisory platform like Betterment to satisfy both customer preferences for a fee. The good news is that the investment management platform is free for anyone to use.

Who should use Personal Capital?

Personal Capital is ideal for anyone who has funds in one or more investment accounts. The tool offers advanced analytics functionality and forecasting tools, letting you review your account fees against recommended averages, simulate how your portfolio might look in the future, and view all of your investments in one place.

It’s great if you:

- Have investments in multiple accounts, or across different assets

- Are curious about what increased portfolio diversification could mean for your potential returns

- Want to review how much you are paying in fees and expenses across your investments

- Want to know where to invest your next dollar to maximize its impact

What are Personal Capital’s strengths?

Personal Capital provides deep insight into your investment performance. It gives you comparison tools to optimize for risk tolerance, return potential or fee structure.

Its strengths include:

- It’s a powerful tool for visualizing your investment accounts. You can view all of your investment holdings in one dashboard and add new accounts with a few keystrokes

- It analyzes how your portfolio stacks up in terms of fees. Fees might not seem important, but a difference of just a single percentage point can save you (or cost you) tens or even hundreds of thousands of dollars over your investing journey

- It can perform complex simulations to predict the size of your nest egg. Using Monte Carlo simulation, Personal Capital will project how much you’ll likely have saved by retirement—as well as the amount you can expect in Social Security income

- It does a great job of telling a visual story about your potential outcomes and how to stay on track with your goals

What are Personal Capital’s weaknesses?

Personal Capital is very good as an online investment manager, but it’s not perfect.

Its weaknesses include:

- It doesn’t monitor your credit

- It doesn’t help you set and monitor your savings goals

- It’s not well-suited to spend tracking as it doesn’t enable you to create your own custom spending categories

- Its automatic spending categorization is not as accurate as Mint’s

- It does not automatically import the last 3 months of your credit card activity to give you spending insights

Mint Review

What is Mint?

Mint is a budgeting, spend tracking, and credit monitoring tool that helps you better manage money in your daily life.

By ingesting and analyzing your financial habits, the platform recommends how you can spend more intelligently or ramp up your savings.

Mint has been around for a long time—since 2006—and today has a claimed 25 million users. Mint, owned by financial software company Intuit, makes money by suggesting specific products and services from other companies, including credit card offers tailored to your credit score; savings or checking accounts; and auto, home, or renter’s insurance products.

Who should use Mint?

Mint is designed to be user-friendly for everyday money management.

It’s a good choice if you:

- Hope to do a better job tracking and understanding your spending

- Want to create a monthly budget (and get notified if you’re close to exceeding it)

- Are interested in saving more consistently

- Would benefit from keeping an eye on your credit

What are Mint’s strengths?

Mint gives you enhanced visibility into your spending and saving habits and helps you keep an eye on your credit score.

Its strengths include:

- It pulls months of account activity to categorize your spending

- It shows your credit score

- It lets you create goals for budgeting–one of the best things you can do to control cash flow

- It displays historical spending trends and real-time transaction reviews

- It identifies products like credit cards or insurance that may be a good fit for you

- It helps you quickly review transactions for fraud

What are Mint’s weaknesses?

Mint, in some ways, is the mirror image of Personal Capital. While Mint is great for budgeting and tracking your spending, it’s also not perfect.

Its weaknesses include:

- It lacks investment portfolio analysis and has features focused on everyday spending

- It doesn’t put your expenses into context the way Personal Capital compares your investment fees to industry averages

- It shows how your investments have changed over time but cannot forecast the future value of your portfolio

How to Get The Most Out of Personal Capital and Mint

Whether you’re using Personal Capital, Mint, or both, you should do the following to get the most out of the platforms:

Link your accounts: When you create a Personal Capital or Mint profile, you’ll be prompted to link accounts from various financial companies (your bank, credit cards, investments). You need to link all your accounts otherwise you don’t get the benefit of a complete personal picture.

Review your spending and net worth regularly: While you don’t need to check your accounts daily, make it a habit to see where you stand at least once a quarter. You can then tweak your savings, spending, or investing mix to better align with your primary objectives.

Set big-picture goals: In Mint, you can set budgeting goals. In Personal Capital, you can set retirement goals (e.g., the age you want to retire or the amount you want to have saved). Whichever tool you use, planning around key objectives will bring more clarity to your financial life.

Use the free planning tools: Both tools offer some great analytical tools like a retirement planner, 401(k) fee analyzer, budgeting tool, net worth tracking, and a cash flow overview.

Other Personal Finance Tools to Consider

Two other options are Quicken and MoneyPatrol, both of which have certain advantages.

Quicken: Quicken is an accounting-focused tool and while powerful, it’s not necessary for your own personal finances. It’s better suited for small businesses or those who need advanced financial management and accounting for their taxes.

MoneyPatrol: MoneyPatrol has many budgeting and expense tracking features, including a helpful calendar view of your expenses. But unlike Mint and Personal Capital, MoneyPatrol costs money: $4.99 a month when you subscribe for a year.

Summary and Conclusions: Personal Capital vs Mint

Personal Capital is best for investment guidance and wealth management, while Mint is superior for everyday money management and monitoring spending on your credit cards.

Mint may be the better choice if you’re interested in becoming a smarter saver, while Personal Capital is the one to choose for advanced investment analysis.

Since both tools are free to set up and use, and each has its own strengths (budgeting and expense management vs investment management), we recommend that you utilize both of them.

Personal Capital and Mint may serve different areas of your financial life, but together they will automate and simplify the process of wealth building.

At Stepwise, we recommend you sign up for both Personal Capital and Mint to take advantage of their respective strengths – no matter where you are in your financial journey.

Disclosure: This article may contain references to products or services that we use and recommend. At no cost to you, we may receive compensation when you click on the links to those products or services. This helps us keep the site free for everyone.

Highly descriptive blog post, I liked that a lot. Will there be a part 2?